Toxic VC and the marginal-dollar problem

October 26, 2017

Venture capital should come with a warning label. In our experience, VC kills more startups than slow customer adoption, technical debt and co-founder infighting — combined. VC should be a catalyst for growing companies, but, more commonly, it’s a toxic substance that destroys them. VC often compels companies to prematurely scale, which is typically a death sentence for startups.

Venture-backed startups face great pressures to perform. The more money raised, the more pressure. One of the challenges well-funded startups face is defining performance. For mostly good reasons, the metric that matters most to VCs is usually revenue growth rate. Particularly for an early-stage startup, this is the right metric, because it is the most basic answer to the question of whether customers care about the company’s product and the company has the potential to become a large business.

Growth at what cost?

Unfortunately, growth without context quickly becomes more of a vanity metric than a success metric. The question that needs to be considered is “growth at what cost?” Few would dispute that growing 3X and adding $10 million in revenue by consuming $1 million in investment is terrific. Likewise, most would agree that growing 3X and adding $10 million in revenue for $100 million in investment is appalling.

Extreme examples are pretty clear; it’s the less dramatic examples that become very confusing. Unfortunately, founders and investors aren’t having the debate about high-quality versus low-quality growth frequently enough, and the wrong incentives can lead reasonable people to catastrophic rationalizations.

Not all growth is created equal. There is “good growth” that supercharges the business and allows for reinvestment into a virtuous cycle, and “bad growth” that ultimately leads to an unsustainable burn and a masked death spiral. Founders always need to be asking themselves, their teams and their investors: “Growth, but at what cost?”

The peril of “go big or go home”

Investors today have overstuffed venture funds and lots of capital is sloshing around the startup ecosystem. As a result, young startups with strong teams, compelling products and limited traction can find themselves with tens of millions of dollars, but without much real validation of their businesses. We see venture investors eagerly investing $20 million into a promising company, valuing it at $100 million, even if the startup only has a few million in net revenue.

Now the investors and the founders have to make a decision — what should determine the speed at which this hypothetical company, let’s call it “Fuego,” invests its treasure chest of money in the amazing opportunity that motivated the investors? The investors’ goal over the next roughly 24 months is for the company to become worth at least three times the post-money valuation — so $300 million would be the new target pre-money valuation for Fuego’s next financing. Imagine being a company with only a few million in sales, with a success hurdle for your next round of $300 million pre-money. Whether the startup’s model is working or not, the mantra becomes “go big or go home.”

The marginal-dollar problem

After this fundraise, everyone at Fuego agrees to hit the gas, hard. Burn rates jump from $200,000 a month to more than $1 million per month. Experiments that previously were returning $1.50 over time for every dollar invested start to return $1 as money is pumped into scale, but everyone agrees that’s okay. It just means that the customer pays back the cost of acquisition more slowly.

As the investment keeps scaling up, soon only $0.80 comes back for every $1 invested. This poor return is upsetting, but growth is the mantra and Fuego’s executives and investors rationalize that this can be fixed later. Eventually, as the company scales further, $0.50 comes back for every $1.

Scale quickly reveals the inefficiency of a startup’s model. But does the overfunded startup take a step back and try to fix the diminishing return of investment? Rarely — until it’s too late. The desperation for growth drives the startup to chase the marginal dollar at increasingly greater costs, enduring rapidly increasing losses. We call this “the marginal-dollar problem.”

Money has no insights on how to fix a broken business.

This develops a habit that is hard to break, and the startup will get worse and worse at solving this diminishing returns problem over time. The problem is further exasperated as the return on most growth investments in startups (more features, more engineers, more support, more brand marketing, etc.) are much harder to quantify and take time to evaluate. The burden to grow at any cost drives the startup to accept exceptionally poor returns on its investments.

How the marginal-dollar problem kills you

Companies are pretty good at knowing what their best “hypotheses” are in product, sales and marketing. Each marginal investment, on average, will perform worse than the higher confidence hypothesis that was previously tested. As a company attempts to unnaturally scale, it will make lower and lower confidence investments that will typically perform worse and worse — all in the name of chasing the marginal dollar. If the startup wasn’t trying to triple an already ambitious valuation, they could proceed prudently, reject investments that don’t sufficiently return and harden their best thesis into a model that generates high-confidence results. Instead, they end up trying to spend their way out of the hole.

To illustrate this challenge with an example that affects many B2B startups, let’s consider the marginal-dollar problem from the standpoint of building a sales force (this is going to get a bit in the weeds — bear with me).

Imagine Fuego’s average sales rep is getting paid $100,000 and is bringing in $250,000 in sales — against a $500,000 target. On the surface, this looks additive — that’s still $150,000 in contribution! Except it doesn’t account for the cost incurred by product, sales engineering, account management, marketing, support, G&A and all the other teams this employee burdens.

Let’s assume the total loaded cost for a rep is $400,000. In a rational world, the cost of these reps couldn’t be justified; however, the CEO doesn’t want to lose that average $250,000 in top-line growth, despite the cost. If Fuego is largely encouraged to “grow at any cost,” losing $250,000 in revenue for each dismissed sales rep isn’t an option.

Worse yet, as the CEO struggles with the underperformance of the reps projecting toward missing the annual sales plan by a large margin, that CEO has a choice of whether to focus on fixing the problem or finding a way to close the revenue gap. How could one make up that gap? Hire more of the inefficient reps? Go big or go home! Sounds crazy, but it’s happening every day in the startup world.

Multiply that scenario across dozens of sales reps (and similar underperforming activities on other teams) and you quickly understand how chasing the marginal dollar of growth can kill a business. As the CEO keeps doubling down on a machine that isn’t working, Fuego shows growth, but at a cost that is unsustainable and will lead to its inevitable failure. This is how big venture rounds kill startups.

Capital has no insights — it is rarely the constraint

Fuego, like many startups, has financed the business on one big assumption — that capital is the major constraint to startup scale. If a company has more capital, it will scale faster. On this assumption, why not raise as much as possible and go as hard as possible at every startup? Our research suggests that this is rarely the case and that the most challenging constraints to growth and success are rarely capital.

Capital can be used to hide these constraints for a period, but typically capital only magnifies the problems over time. Money has no insights on how to fix a broken business. Great businesses solve these problems first and then use capital to intelligently scale models that are clearly working.

We’ll fix it as we scale

We often hear founders and investors argue that the problems in their companies can be fixed as the company scales. It’s not hard to imagine Fuego acknowledging the major problems with the economic engine of the business, but rationalizing that capital can be used to both scale the model and fix the model at the same time. This is very seductive logic, because it allows everyone to keep playing the grow-at-any-cost game while pretending that the problems will get solved later.

Unfortunately, we almost never see this work (for fairly obvious reasons). Scaling a business is hard and nearly always yields less efficiency over time. It takes so much effort to scale without losing yield on nearly any productivity metric that the dream of scaling while increasing productivity is typically a mirage.

Sell the dream, buy the nightmare

From the outside it’s so obvious — Fuego needs to hit the brakes. Returning $0.50 for every $1 invested cannot be fixed at scale. Unfortunately, in the pursuit of growth, people lose focus on the costs until it’s too late.

Fuego’s VCs invested with the goal of building toward a billion-dollar exit. They invested because they believed in Fuego’s potential — why would they go slow? That would be admitting to themselves and everyone else that the investment thesis was invalid. They convinced the partners at their funds that this was going to be the next home run; how can they pause now?

Every attempt at scaling up an inefficient experiment dramatically decreases the likelihood of success for a startup.

The burden on the founders is immense. The founders sold the VCs on this billion-dollar future. How can they get cold feet now that the cash is in the bank, even if the model is broken? If they cut back on the burn, talented people will get the sense the company’s prospects are dimming and leave. Appearances must be maintained!

This works for a while — everyone is drinking the same Kool-Aid — until the company needs to ask its investors for more money and inevitably hits the enthusiasm gap. One reason that scaling a bad experiment is so detrimental in the long term is that the incentive to keep scaling doesn’t go away, but the investors often become unwilling to fund it when the company inevitably runs out of cash.

Build a better engine or hope not to explode

Every attempt at scaling up an inefficient experiment dramatically decreases the likelihood of success for a startup. Capital is a multiplier of the good and bad at a startup. A startup can use capital to compound activities that are working or compound activities that are not working. Unfortunately, venture capital often drives founders to do that later. It is incredibly difficult to fix the multiplication of bad mistakes. This is why VC is so dangerous: venture capital incentivizes companies with good vanity metrics to start scaling bad experiments.

Think of your company as a car in a race to cross the country with an engine that’s leaking gasoline. The faster you accelerate the engine, the more the car leaks and the greater the risk of explosion. You have two options. You can slow down the car, pinpoint the problem and fix it; or, you can just keep pouring more gas into the tank, hoping for an infinite supply, and accelerate at maximum speed — all the while praying that the fuel leak doesn’t lead to a catastrophe along the way. So the car goes faster and faster with a decreasing rate of efficiency and an increasing probability of tragedy.

So about that warning label, perhaps it should be: “Founders: Burn Responsibly.”

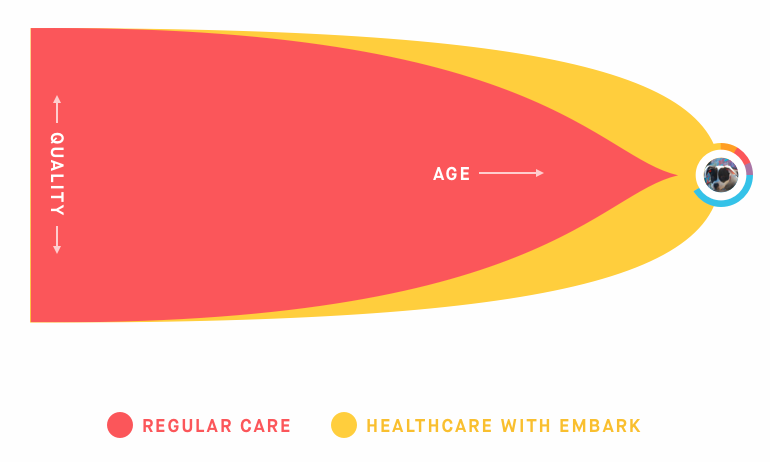

Github for Greyhounds: Our Investment in Embark

July 18, 2017

Snorkie, Miniboz, Cavazoo, and Scoodle would all be passable startup names, but they’re actually relatively new canine crossbreeds and represent just a fraction of the entrepreneurial energy recently invested in designer doggies. The Labradoodle, a hypoallergenic mix of Labrador retriever and poodle, the favorite dog breed of Miley Cyrus, the Norwegian crown prince, and the Paley family, only bounded onto the scene in 1955. Humans have domesticated dogs for 15,000 years, but the first Silken Windhound wasn’t born until 1987. Like web portals, Chiweenies (that’s a Chihuahua/Dachshund mix), achieved huge popularity in the early 1990s.

We live in a heyday for hybrid pups and that’s why we’re proud to announce our investment in Embark, a service that deciphers doggy DNA for pet owners, breeders, and vets. Think of it as Github for Greyhounds.

For just $199, Embark provides a report that calls out hundreds of interesting facts about your pet — everything from its geographic origins to a dossier on the personality traits it is likely to display. Consumer genetic testing is an amazing tool for genealogists and has fascinating long-term potential for modern medicine, but Embark moves in dog’s years. The Embark test can lead to a stronger, healthier litter of puppies in as little as two months and can shift the longevity of a breed in only a decade!

How Does Embark Help?

1. Pet Owners: There are 72 million dog-owning households in the US which spend over $66B on their pets each year. Besides offering incredible new insights on the origins and genetic makeup of a beloved family member, Embark can help golden retrievers better enjoy their golden years by giving owners a heads up on the maladies their mutts are genetically susceptible to and which foods and interventions might serve them best. Who wouldn’t want to give their best friend a longer and healthier life?

2. Veterinarians: There are 26,000 small veterinary clinics in the US. Vets armed with DNA test results will be able to more accurately diagnose the health risks their patients face and offer proactive solutions. Moreover, Embark is creating a genetic database of dog DNA which will surely lead to new discoveries in veterinary science.

3. Breeders: The benefits to breeders extend far beyond those that want to pioneer the next bespoke breed. With Embark, purebred breeders can use science rather than superstition to declare the pick of the litter and further refine the breed’s family tree. By investing in a DNA bank that will help improve the health and longevity of a breed, breeders can ensure the value of their dogs and businesses for generations to come.

Beyond the benefits to pet lovers and vets, Embark is a model of what we look for in a startup:

The Founders are Best in Breed

(Almost No One Else Could Start This Company)

There is a reason Airbnb and Facebook were started by recent college grads. TJ Parker, a 2nd generation pharmacist who loves tech and obsesses over user experience, is the perfect person to lead PillPack.

Outsiders can bring a useful perspective to markets, but all things being equal, we’d prefer to back founders who fit their markets. Co-founders Adam and Ryan Boyko are uniquely suited to understand dog DNA. Adam is a Professor of Veterinary Medicine at Cornell University with 41 journal articles to his name. Ryan studied Computer Science at Harvard and epidemiology at Yale. Together, they’ve been swabbing dog cheeks for years and have traveled to Peru, Uganda, and Egypt in pursuit of rare breeds to build out their model. How many teams out there have members that delved into doggy drool to earn a doctorate, the ability to design a database, and a demonstrable knack for consumer-facing design?

They’re Barking Up the Right Tree

(What we Mean by Weird and Wonderful)

We talk a lot about funding “weird and wonderful” businesses. People often take it to mean we favor or seek out bizarre-sounding ideas, but that’s a superficial read. What we look for are founders who see a crystal clear use case hidden in an industry or market that is opaque, or downright frightening, to most people and far from a current venture capital theme. We rarely invest in hot new technology platforms for their own sake, but we are willing to back great use cases that happen to operate in weird industries.

They’ve got a Nose for Business

(Good Founders Like Talking About Hard Problems)

To be honest, when I was first introduced to Embark, I was a bit skeptical; however, Ryan backed up a barking mad pitch with a barrage of information about the business and its early traction and market adoption.

And their success isn’t just a matter of sales. In a short period of time, Embark has truly become the leading DNA testing product for dogs despite that competitors have been around for years. Ryan and Adam are regularly interviewed by the New York Times, National Geographic, and other national publications as they’ve done a world-class job establishing their thought leadership on canine genetic health. They’ve done creative business development deals, like designing quizzes for the Washington Post and providing the genetic testing for the annual Puppy Bowl. They might be the most media-savvy pair of scientists I’ve ever met. It’s easy for science-focused teams to handwave past the tricky business issues, like pretending to throw a tennis ball to a Beagle, but the Boyko brothers have done the hard work of building a real business around their technical breakthrough.

Some people say all deals have fleas, but we’re wildly wagging our tails about leading this round of funding alongside Shana Fisher at Third Kind, Jenny Lefcourt at Freestyle, Bill Maris at Section 32, Anne Wojcicki who made a personal investment, and couldn’t be more excited to welcome Embark to Founder Collective!

There’s No Shame in a $100M Startup

June 15, 2017

The era of unicorn startups has created a distorted view of entrepreneurial success. All the talk about billion-dollar exits has inflated the numbers that define a win. Starting and selling a company for $100 million dollars is an outlier event in terms of pure entrepreneurial probability, but such outcomes are viewed as well short of success in many corners of today’s startup world.

This bizarre belief isn’t universal, but a surprising number of VCs and industry observers are thoroughly unimpressed by low nine-figure exits.

In our hype-driven society, this actually isn’t so surprising. Political reporters want to write about the president and the Supreme Court, not state government. Likewise, tech journalists want to write stories about companies that spell million with a “B.” Investors at billion-dollar funds want to deploy $50 million into winning companies, and $100 million exits are seen as consolation prizes instead of reasons to cheer. In this echo chamber, a $100-plus million exit seems like a jumbo-sized acqui-hire.

To put this reality distortion into context, we examined the outcomes of a special segment of the successful founders over recent decades — those who have become VCs. Looking at a broad cross-section of top VC firms, we identified 63 investors who have a background in starting companies. Only 11 of those founders-turned-investors have built enterprises that have IPO’d or sold for more than $1 billion.

Many of the most successful investors built exceptional startups, which only by today’s distorted standards look like “modest” economic outcomes. Y Combinator’s Paul Graham is one of the most influential venture capitalists of the last 10 years, yet his startup Viaweb sold for “just” $49 million. Viaweb was a success by any realistic standard, but perhaps not by today’s hyped success narrative and fundraising stockpiles. The company only raised $2.5 million before its sale — a pretty impressive return and an amazing precursor to what was to come for Paul Graham. It turns out that “small” exits can lead to big things.

Note: This isn’t an encyclopedic list, so if we missed someone, please let us know. Also, some of the dot-com-era exits are hard to value accurately, but citations are available. In the case of undisclosed amounts we assume the acquisition prices were lower than the materiality threshold of the buyer.

Belittling $100M success stories

Not only is selling a company for $100 million often scoffed at by VCs, at times it is outright mocked by the startup community. Aaron Patzer became famous for building Mint.com, and the site’s powerful UX was such a breakthrough that Intuit paid $170 million for the company. He didn’t buy into the “go big or go home” ethos; instead, he earned a fortune — and was roundly ridiculed for it. The disdain for “small” $100 million sales is so strong there’s even an Urban Dictionary entry for selling your startup for too little money — it’s called “Pulling a Patzer.” No seriously, go look it up. We’ll wait.

One of our portfolio companies recently sold to a tech giant for just over a hundred million dollars. The acquisition gave us an exciting multiple in a short period, and each of the co-founders made more money than LeBron James last year. This sale was quite possibly the best realistic outcome the company could have expected and a huge win for all parties.

In this unicorn-obsessed startup era, the lack of appreciation for these victories is a failure of vision at best, and unfortunate cynicism at worst.

“Go big or go home” is broken logic

We’re not suggesting entrepreneurs should look for quick flips or undervalue their company’s potential. We want to fund the next Uber, Google and Facebook. The reality is that not every business is suited for that. Part of the reason so many of these VCs had great outcomes at well below unicorn fantasy levels is that they raised the right amount of money for their businesses at valuations that maintained exit options.

Ideas that look like billion-dollar businesses at the seed stage can run into unexpected barriers. For modestly funded startups, these mistakes don’t need to be fatal. Unfortunately, most VCs are sized such that they can only succeed if they have several companies in their portfolio exit for more than a billion dollars. So VCs overfund startups with decent but uninspired progress, which cuts off realistic and enriching exit opportunities.

For example, you might have a company with $10 million last year in gross revenue that earned a $50 million valuation in its last round. This company hopes to double its revenue this year and is in a sexy category, but it has thin margins and a loose handle on its unit economics. In a normal environment, that company might raise $20 million on an $80 million pre-money valuation as the next step up.

Instead, in the current climate, a VC will see signs of progress, get excited by the market and convince the founders to “go big or go home.” This VC has $20 million burning a hole in his pocket (he needs to deploy this capital to raise his next fund) and convinces the entrepreneur to take $40 million (with half to insiders) on $260 million valuation instead. Now, with a $300 million post-money valuation, the company needs to sell for a billion dollars to be worth the VC’s time.

With only $10 million in revenue and very thin margins, the company has sold its option of a $500 million exit. If they had raised less money, a sale for half a billion dollars would have made everyone happy. Instead, they’ll probably increase their burn rate and raise more money. Eventually, this promising company could possibly go out of business when no acquirer wants to pay the inflated price and VCs lose interest in funding the excessive burn rate required to continue to fuel false hopes.

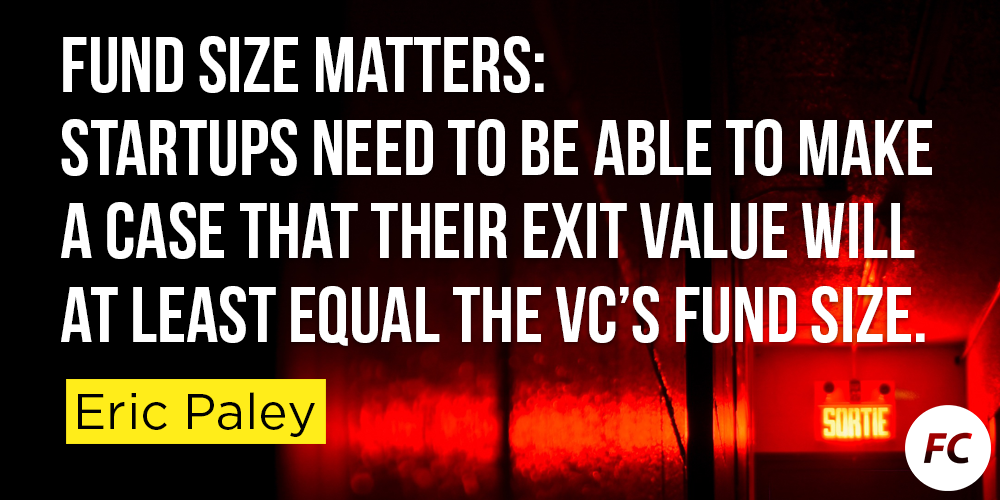

Fund size tells you everything

A lucrative $100 million exit is only possible if you don’t over-capitalize your business. If you want flexibility, you’ll have to fundraise strategically. This starts with choosing your investor. Founder Collective partner David Frankel often says, “fund size tells you everything.” As a very rough rule of thumb, your startup needs to be able to make a case that it can exit for at least the value equal to the size of the VC’s fund. Raise from a $50 million fund, you can sell for $100 million easily. Raise from a billion-dollar fund and you need to shoot for the moon. Choose carefully and make sure you know what you’re signing up for.

There’s no shame in a $100M startup

The vast majority of tech companies are sold for less than $100 million dollars. Raising a relatively small amount of money and selling a company for $100 million dollars should be celebrated. For most founders-turned-VCs, this was the definition of success when we sold our own companies. In some cases, selling for tens of millions of dollars can be more lucrative for founders than selling for hundreds of millions, or even billions of dollars.

Selling a relatively successful startup can create enough wealth to allow you to live comfortably for the rest of your days. It can put you in prime position to start another company — or perhaps the leading accelerator in the world. Many founders turn “modest” successes in the entrepreneurial realm into amazing careers in venture capital.

Welcoming Andy Palmer

May 3, 2017

Today, we’re proud to announce that Andy Palmer has joined Founder Collective as our newest Founder Partner (and be sure to read Andy’s post explaining his motivation for joining FC.) David Frankel recently explained what we look for in this role: entrepreneurs who are wholly-focused on building their own companies and partner with our firm on a part-time basis to invest in other entrepreneurs (and in Andy’s case, the Cambridge/Boston startup ecosystem).

Founder Partners are magnets for talent, insatiably curious, deal-savvy, and experienced angel investors. Andy couldn’t be a better fit for Founder Collective, as I detail below. For Andy, Founder Collective will help him continue the mission he started with Koa Labs — to support the Boston/Cambridge entrepreneurial ecosystem — while he maintains his primary focus as the CEO at Tamr, the company he co-founded with his partner and Turing Award Winner, Mike Stonebraker, PhD.

Andy built a unique career combining tech, life sciences, and data engineering that included serving as:

- VP of Sales and Marketing at pcOrder.com during the dot-com boom

- Chief information and Administration Officer at Infinity Pharmaceuticals

- Co-founder and founding CEO of of database company Vertica (sold to HP)

- Global head of software and data engineering at Novartis Institute for Biomedical Research

- Founder of Koa Labs, a seed fund in Cambridge where he supported the founding of such great companies as PillPack, Recorded Future, Evergage, Kinsa, Desktop Metal, and dozens of others

- Most recently co-founding Tamr, a data unification platform that reduces the time and effort to connect multiple data sources, with funding from NEA, Google Ventures, HPE, Thomson Reuters, GE and MassMutual

Andy is a nexus for entrepreneurs in Boston, and I’ve seen him change people’s lives and career paths by leveraging his experience and networks. The following attributes are just a small part of what makes him special.

Mission-driven

Andy learned how to program writing computer games in the 1980’s as a teenager. His love of computers and software has driven him throughout his career and fueled his personal mantra: “Getting paid to play with computers and software all day is too good to be true.”

Andy’s inspiration for being an entrepreneur came naturally: “My grandfather was an entrepreneur. He sold firetrucks — he loved everything about cars and big trucks. He supported our family, was an amazing role model and he got to play with trucks all day. I’m really just trying to be like my grandfather — but with me it’s computers instead of trucks.”

A Role Model

Andy is a sharp, deal-savvy investor, but he’s also one of the most generous people I’ve met in the Boston ecosystem. He’s made more connections that have led to lucrative deals and momentous career changes than most of the recruiters in Boston. Many investors use favors and intros as a form of currency while Andy proactively offers help with no expectation of return with great regularity. Personally, he’s been a role model for how to catalyze a startup community. Andy credits his long time partner and close friend Frank Moss for his behavior: “Frank taught me how to be a great entrepreneur while also being a great person and caring for others.”

Tech + Life Science + Consumer + Data

Like us, Andy looks for unique individuals working to solve compelling problems with focused use cases. More specifically, he’s deeply focused on the intersection of tech and data, with a special interest in companies that combine them with life sciences and consumer applications.

He’s all over these issues at Tamr and is working hard to improve the quality and actionability of data for his customers, explaining that “companies have spent 40 years collecting data, now they’re trying to use it. One customer thought they had a two hundred thousandmillion customers. It turned out they had half that number. If you’re wrong about your data is inaccurate, how do you do anything useful with it?”

Founder First

One of the many reasons we’re honored to have Andy on the team is that he has never been an institutional venture capitalist. Why? He loves building companies and playing with tech too much to give it up.

We designed our Founder Partner program precisely to accommodate polymaths like Andy so they can support other founders without letting go of their true passion and their primary interests. This structure gives entrepreneurs who take funding from us access to a team of professional investors that can help with general strategy, fundraising, etc. as well as founders like Andy who live and breathe big data and can offer deeper domain expertise.

“Entrepreneurship is a team sport; I believe that with my soul,” he says.

Humility

Humility and empathy with founders are core values at our fund. Andy is a kindred spirit in this regard. At Tamr, there are no assigned desks, and he’s as likely to be found at a table at a cafe as in an office.

When he built his co-working space, Koa Labs, the same thinking was at work. “We were very deliberate in building something rough around the edges,” he says. “One of the problems with most co-working spaces is that they’re too nice. You need intimacy, a rough lifestyle. You’re trying to do things that shouldn’t happen in a rational world. It’s hard to do that in a space that feels like corporate America.”

Andy rejects the notion that investors are kingmakers — it all comes down to the entrepreneurs. He elaborated “so many venture firms use a rule book devised by the early players in the business. They have all these assumptions about how much ownership they should have, what backgrounds founders should have, and most institutional venture investors have sold those assumptions to their limited partners. I believe we should question more of those assumptions. We don’t have to use that playbook. When you break the rules, question dogma, that’s when you get outsized returns. Coming out of grad school I worked for Joe Liemandt at Trilogy in Austin, TX. Joe is great example of an entrepreneur who doesn’t conform to other’s assumptions. I learned so much working for Joe at Trilogy.”

Welcome to FC Andy!

Overdosing on VC: Lessons from 71 IPOs

October 20, 2016

Venture capital is a hell of a drug. Used properly, it’s like adrenaline energizing many of the greatest companies of the past fifty years. Used incorrectly, it creates toxic dependencies.

The conventional wisdom in the startup community is that when building the very best companies, more capital can be leveraged to accelerate even greater growth. But does this “go big or go home” approach stand up to scrutiny? In the best case scenarios, do companies that load up on venture capital actually outperform those that more efficiently deploy capital? We looked at 71 tech IPOs from the last five years to find out.

Efficient Entrepreneurship

At Founder Collective we’ve been talking to our community about the virtues of what we call “efficient entrepreneurship.” We’ve written recently about the downsides of heavily funded companies, including the loss of exit optionality, and perils of unsustainable burn rates, but how does aggressive venture capitalization look on the upside? By studying the best cases of venture capital success, what can we learn about the benefits of raising lots of money?

The results were surprising — by examining the technology IPOs of the past five years, we found that the enriched (well capitalized) companies do not meaningfully outperform their efficient (lightly capitalized) peers up to the IPO event and actually underperform after the IPO.

Raising a huge sum of money is a requirement to join the unicorn herd, but a close look at the best outcomes in the technology industry suggests that a well-stocked war chest doesn’t have correlation with success.

Of the 20 most successful publicly-traded startups over the past five years (measured by current market cap), 14 raised in the neighborhood of $100M or less. Six raised less than $50M. One raised no capital at all. These are shockingly small amounts of money when you consider the median privately-funded unicorn has raised $284 million dollars.

Methodology

Evaluating startup performance is a messy business. Late stage companies are rightfully secretive. Acquisitions are messy financial affairs often engineered to obfuscate the true value of a transaction. The IPO market was the most transparent proxy we could find, and while imperfect, it is instructive. With notable exceptions, most of the biggest outcomes in venture capital are a result of IPOs. By studying the relationship between venture capital and IPOs of the past five years, we can get an idea of whether raising more capital in the best companies correlates to better outcomes.

The Data

- The data includes 71 companies that raised a total of $10.2B in venture capital

- Their combined market cap is $566B, or 55X the capital invested

- The average startup on the list raised $144M in VC to build a company worth$7.9B

- The median startup on the list raised $79M in VC to build a company worth $1.8B

Pretty exciting results overall! Of course this data set reflects nearly all of the best outcomes in the venture industry over the last five years.

Setting Facebook Aside

Acknowledging that there is only one Facebook and that it is an extreme outlier among outliers, we excluded the company from most of our analyses. Absent Facebook, the overall numbers still look pretty strong, but it is astounding to see how much one company skews the totals:

- 70 companies that raised $9.6B in venture capital

- Their combined market cap is $202B, or 21X the original investment

- The average startup raised $137M to build a company worth $2.8B

- The median startup on the list raised $79M in VC to build a company worth $1.8B

Exclusions

We only looked at companies that held IPOs between 2011–2015. It would be interesting to go back further than five years, but it is also instructive to examine what is effectively the “unicorn era” in which private companies raised unprecedented amounts of capital. We excluded companies that were founded prior to 2000 (e.g. GoDaddy, FirstData), companies with unorthodox financing paths (e.g. Match Group, RetailMeNot), and companies in Asia and Russia, because they have significantly different financing environments. The result is a dataset, available for review, that includes 71 companies. Most of the data was taken from Crunchbase, except where noted.

We also excluded late-stage private equity, secondary offerings, and debt from the calculations, though they are recorded in the spreadsheet. We were less interested in the money raised in the IPO, as we viewed as a graduation point from the venture capital game and is largely a direct function of company size. The data certainly contains imperfections, though we did our best to get it right, and we’re open to feedback on the dataset, which is why we’re making it public.

The Best Case for “Big VC”

This data might suggest that “go big or go home” makes some financial sense, especially for investors. The most heavily funded companies do have larger total dollar returns. Counted together, the 20 best funded companies on the list raised $6.7B in VC and have an aggregate market cap of $62B, for a ~9X return.

The 20 least funded companies on this list only raised $623M in VC, yet managed to return $48B to investors, or an 77X return.

That’s a $14B dollar difference in aggregate returns. That’s non-trivial, especially to VC as an asset class. However, ~$12B of that difference is accounted for by Twitter, who raised a little less than a billion dollars in VC. So aside from those Facebook and Twitter, venture capitalists spent ~$5B to make an incremental $1B. It’s important to note that the stock market is volatile and that over the course of writing this post, the 20 most enriched companies have fluctuated dramatically. Still, the variance is usually driven by one or two outlier companies.

It is true that there are a few companies founded each year that drive the bulk of the returns. It is also true that in the case of only a couple of outliers (Facebook and Twitter), heavily funding the best companies is a winning strategy for investors. However, It is not clear that VCs have been able to consistently identify the best performers and have instead overfunded even the most successful companies.

This isn’t a knock on the VC model — it’s an asset class predicated on risk. The best firms in our industry have shown an ability to run this high risk playbook over many funds.

It should be a lesson for founders though. Companies like Facebook and Twitter are critical for the health of the ecosystem, but are not a good model for other startups. Unless a founder is very confident that they are building the next Facebook scale business, they would be better served focusing on creating higher multiples instead of a higher exit value.

VCs Have a Portfolio, Entrepreneurs Get One Shot (At a Time)

VC can afford to risk overfunding a dozen companies in order to be a part of the epoch-defining winners, but entrepreneurs only have one shot. As a founder, are you willing to take 4X more risk for what, even in the best cases, results in a 24% premium? That’s basically what the companies on the top of this this list did:

- The median enriched startup raised $193M to build a company worth $2.1B

- The median efficient startup raised $37M to build a company worth $1.7B

The financial calculus for founders is even worse than it appears. Incremental funding will probably come with extra dilution, and pre-IPO preferences that will favor the VCs if the startup’s hot streak falters and it doesn’t get public. Beyond the magnitude or risk, more capital limits the number of possible exit paths. The founders of the 20 most efficient companies likely could have successfully sold their companies at any point along their development for a healthy return. Their enriched counterparts are locked into billion dollar exits with diminishing returns on capital.

Is this actually the best model for VCs?

It’s conventional wisdom in the VC market that investors should heavily lean into their winners, but are you better off doubling down on winners for diminishing returns or funding a new crop of startups with the potential to return 10, 20, or 30X?

Davids vs. Goliaths

Though it’s a ridiculously small sample, look at companies that raised an objectively large sum of money — say over $200M (nine companies in this sample), versus an equal number at the bottom of the list. The results are staggering:

- The most enriched companies raised $567M to return $3.5B or 6X

- The most efficient companies raised $12.9M to return $2.8B or 218X

- The most enriched companies raised 44X more money to get a 25% better return

Power laws in venture capital are real, but fundraising is a poor predictor of them. A couple of great companies raised a lot of money, but more money doesn’t make runaway successes any more likely. If you exclude Twitter as well as Facebook, the top 10 most efficient startups actually outperform the 10 most enriched companies.

Less Money = Better Companies?

Market value at the IPO is important because it is often a marker of the venture capital exit value, but it’s also interesting to consider how these enriched companies compare to their efficient peers in the long term as public companies. Does instilling a sense of fiscal restraint early, where growth comes from disciplined customer acquisition, not a venture capitalist’s checkbook, lead to more sustainable businesses?

It turns out the efficient companies have performed significantly better as public companies than the enriched group:

- The 20 most efficient startups have appreciated by 89% since their IPOs

- Their enriched counterparts only grew by 22% in the same period.

This trend is even more startling from a modal perspective:

- 8 of the 20 most enriched startups have actually declined in value since their IPOs

- Only 3 of 20 of the most efficient companies have lost value since their IPOs

Our hypothesis is that too much capital over time creates a culture that substitutes cash for creativity and operational discipline. Big balance sheets allow companies to grow inefficiently, to paper over problems with headcount and spend, rather than confronting the core engine of value creation. Having less money forces a management team to make hard decisions early on and to cut off potentially wasteful problems that otherwise could linger indefinitely. This efficient ethos becomes part of the long term culture of productive performance that is difficult to infuse in the enriched companies that never operated in a constrained way.

There is a fair counter-argument that the enriched cohort had higher valuations at the time of the IPO and that the value was captured by private market investors rather than public investors. While possibly true, entrepreneurs and VCs should consider the implication of this argument is that public market investors may apply significant discounts to the increasingly large unicorn club that has raised large amounts of private capital prior to an IPO.

Shouldn’t There be a Positive Correlation?

It’s important to take a step back and consider how surprising this data set really is. The venture capital industry accepts as an assumption, that in the best outcomes, more money accelerates more success. Some would argue that it’s nearly impossible for a true winner to be overcapitalized — these companies are reinvesting the capital into their success economic engines after all. Capital gives you the ability to make more investment in drivers of the business — talent, R&D, customer acquisition, etc. Intuitively, it makes sense that enriched companies should do better than their lightly funded counterparts.

We would have expected to see correlation in these numbers and be debating the embedded causality assumption that we assume in the venture industry. In other words, we’d expect to debate whether the money caused the success (causality), but take for granted that the most successful companies were in a position to raise the most money (correlation with unclear causality).

It’s shocking that no meaningful correlation is present in the data. Although the best performing companies are in the best position to raise the most capital, they don’t necessarily do so.

With the exception of a few critical outliers, the better funded companies aren’t meaningfully bigger or better performing and actually become worse public companies. VC is an outlier business, a vocation premised on volatility, but the fact that highly-funded companies aren’t clearly outpacing their cash-restricted competitors shows there is a point of diminishing returns for capital even among the very best companies. The data suggests that VCs struggle to understand where that point is. The adage in VC has been that there are only 15 companies born every year that matter. If loading cash into companies is your game as a VC, it appears that there are only 2 companies over the past 5 years that actually mattered. That’s a nearly impossible game to play.

What About Acquisitions?

It would be fair to object that we’ve excluded acquisitions from this analysis, but they likely would have strengthened, not weakened, the conclusion. It turns out that many recent billion dollar plus acquisitions were efficient with their capital, e.g. WhatsApp ($60.25M), Oculus ($93.55), Nest ($80M), Instagram ($50.5M), Twitch ($35M), Cruise ($18.8M). Mojang — the makers of Minecraft — skipped fundraising entirely before a multi-billion dollar sale to Microsoft. Beats ($300M) and Jet ($565M) are exceptions in this group, but these companies dramatically underperformed their peers in terms of multiples.

Imperfect Data, Clear Results

We know this analysis is imperfect. Some of the companies that IPO’d in 2015 haven’t yet reported four quarters as public companies and even if enriched with VC, might have more positive long term results. Still, this data should give founders and VCs pause. Though increasingly unfashionable in the unicorn era, it is quite possible, and perhaps even advisable, to build a billion dollar publicly-traded company with under $50M in venture capital.

Looking at the data, 15 of the 20 best performing startups of the last five years raised less than $125M from venture capitalists. (We’re including Wayfair in this tally, which didn’t raise any capital for the first 10 years of the company’s life and whose deal was more akin to late stage private equity). Four, Atlassian, Shutterstock, Textura, and SkullCandy succeeded with no venture capital whatsoever. Splunk and Palo Alto Networks, combined, raised approximately $105M and currently have a shared market cap greater than $20B. Groupon and Zynga each raised multiple $100M+ rounds, nearly $2B in total, and are currently worth ~$5B.

Capital Raised Is a Vanity Metric

Fundraising is a strategic choice that needs to be as carefully considered, just like your product roadmap, marketing strategy, or hiring plan. Unfortunately, entrepreneurs tend to make funding decisions opportunistically, or even worse, out of a sense of pride or false validation.

If you’re enjoying success, money will be thrown at you. It’s flattering and having a strong balance sheet can be a good thing, but it does limit optionality and creates more difficult exit paths. Capital is rarely your biggest constraint or the biggest opportunity in front of you. Worst of all, the evidence shows that there is a limit to how much your balance sheet will help the long term value of your company even in the very best outcomes. Putting this data set in perspective, while the enriched companies underperformed, they were modestly financed compared to today’s unicorns. Our median enriched company (top 20 in terms of capital) raised $193M before going public. Today’s unicorns sit at a median of $284M in capital raised and they may yet need to raise more money to reach the public markets. Our data suggests that this is not a positive sign for long term success. Buyers beware!

The point of this isn’t to encourage bootstrapping; nor is it celebrating slow growth. We’re not advocating a “Just Say No” position on raising venture capital — we’re VCs after all. Though some companies are able to achieve huge success without fundraising at all, they are very unusual. Startups don’t get bonus points for trying to build a company on hard mode.

The founders of these efficient startups had the same ambition and hunger to build businesses as their enriched counterparts. They just did a better job of it. These more efficient entrepreneurs are building real, international multi-billion dollar organizations with far less risk and likely own much more of their companies. The surprise in this analysis is that it appears likely that being capital constrained to some degree was helpful, not harmful, in that journey.

This Isn’t an Attack on VC. It’s a Celebration of Entrepreneurs

The mystique of entrepreneurship used to be in the magical act of making something from nothing. Now, we celebrate founders who act like banks by raising huge sums from venture capitalists. We think this is unhealthy and needs to change. While the startup market has been flooded with capital, founders don’t need to raise huge sums to be successful, and it seems that even in the highest upside cases, raising less money leads to better companies. Yet today, most founders are convincing themselves to take the opposite approach.

We’re making an argument for the efficient use venture capital, not against the use of venture capital. Venture Capital is an essential ingredient in the success of many startups, and there are rare times when adding huge amounts of capital is justified. But like most drugs, there is a time and place for their use and the side effects should be clearly noted to potential users.

Our portfolio contains a number of companies that have followed the enriched model and others that were so efficient that they seemed fueled by the scent of a petrol soaked rag. The advice for both is the same. Think about how you would run your company differently if the money in the bank was the last you’d ever get? The answer to that question could make you a billionaire.

Venture capital is a hell of a drug

September 16, 2016

There has been a lot of money sloshing around the startup world for the past few years. Cheap and accessible capital has advantages: More founders get the opportunity to pursue big dreams and previously “unfundable companies” not only raise huge amounts of money, but some ultimately achieve unicorn status.

Discussions about the downside of this trend are usually related to systemic risks, like the perpetual bubble talk, but few are discussing the problem as it relates to founders — more capital equals more risk. But who is bearing this risk, and what really is the downside? Sure, capital providers are taking this risk — but they aren’t the only ones.

Venture capital increases risk for founders

On a short-term basis, raising VC reduces a founder’s personal risk by allowing the team to draw a salary. Founders don’t need to put development costs on a credit card or face short-term economic hardship. But while counter-intuitive, raising venture capital makes your startup riskier in two key ways.

You limit your exits

VC cash comes at the cost of reduced exit flexibility and the burden of an increased burn rate. Viewed probabilistically, the most likely positive exit for a startup is an acquisition for less than $50 million. This outcome has little benefit to VCs, and they will happily trade it for an improbable shot at a higher outcome.

Think of venture capital as a power tool — in the right hands, power tools can solve some real problems.

I regularly see entrepreneurs agonize over a percent of dilution, while ignoring the fact that they are surrendering their most likely exit options for a low-probability shot at building a superstar startup. Billions of dollars have been outright wasted by founders selling future value that didn’t materialize, while surrendering present value that could have been navigated to great success. My advice: Don’t give up your present for a future you haven’t validated.

You increase burn to dangerous levels

Beyond signing away exit options, new venture capital typically is raised to fund higher burn rates. That increased burn rate is a great investment when it is being used to fuel a model that is working. More often, the increased burn is used to search for a model that works, and the company quickly learns that capital has no insights; it’s just money. Then the company cannot sustain the burn, the CEO decides to cut the burn way too late and cannot manufacture enough VC enthusiasm to keep the dream alive.

Every dollar you spend is a dollar of dilution. One rough rule of thumb is that startups should be able to triple their post-money valuation in two years. If you can’t figure out how to get 3X leverage on every dollar you spend, you’re better off not spending the dollars — or raising them in the first place.

Founders need to think of venture capital as a power tool — a fairly dangerous one — but instead often mistake it for some magical, infinitely renewable resource. In the right hands, power tools can solve some real problems. Used incorrectly, they can chop off your hands.

VCs need billion-dollar exits — you don’t

Billion-dollar exits are brilliant, but they shouldn’t be how founders calibrate success. The mania for billion-dollar valuations is the result of the business model of the venture capital market — not some legitimate definition of startup success.

Here’s a very rough illustration of billion-dollar VC fund logic:

- VC raises a billion-dollar fund, needs to triple the fund to be successful

- VC makes ~30 major investments

- VC breaks even on 10, loses money on 10, needs remaining 10 to be worth an average of ~$300 million in proceeds to their fund

- VC can only expect to own 20-30 percent of any given company (often less); anything less than $1 billion exit of your business isn’t a success in this model

This is why there is so much focus on billion-dollar exits. Not because this outcome is high frequency, but because a few massive funds need it to be so. Let’s not just point fingers at the billion-dollar funds. Similar VC math causes irrational trade-offs for founders whether their investors have billion-dollar funds or quarter-billion-dollar funds.

Capital has no insights; it’s just money.

As a general rule of thumb, assume that your exit needs to be approximately the size of the VC fund to “matter” in its returns. Of course, this is the tail wagging the dog, as the capital gatherers are encouraging irrational behavior of founders with a sales pitch of “go big or go home.” No one says the truth, which is “go big or ruin your life.”

When your business fails, which probability says it most likely will, that VC has 29 more shots on goal. You destroyed your single startup, not to mention the wasted sacrifice over years of your life. In most VC deals, the investor is taking much less risk than the founder.

This is just fine for a subset of founders. It’s great that Ferraris exist, but it doesn’t make sense for the average person to mortgage their home and their future to buy one when a Toyota Prius can fetch groceries just fine.

Exit value is a vanity metric

If one of your goals is making money, focusing on the exit price is a bad idea. It’s quite possible to sell a startup for a billion dollars and make less than someone who sells theirs for $100 million.

For example, the Huffington Post was reportedly acquired for $314 million, and Arianna Huffington made about $18 million. Michael Arrington sold TechCrunch to the same buyer for $30 million and reportedly kept $24 million. To a VC, TechCrunch’s sale would have been a “loss,” and many VCs would have pushed Michael not to sell. Yet Arrington was more successful, financially, than Huffington.

Practice efficient entrepreneurship

One argument I’ve heard from many VCs is that a founder won’t build a billion-dollar startup unless they go all-in from the start. This is nonsense — to become a billion-dollar business, a founder first needs to build a $10 million business. Founders shouldn’t jump to the end game before they’re ready. You focus on the first step and still become a huge player in the end.

Don’t give up your present for a future you haven’t validated.

This is empirically true — just look at Wayfair, Braintree, Shutterstock, SurveyMonkey, Plenty of Fish, Shopify, Lynda, GitHub, Atlassian, MailChimp, Epic, Campaign Monitor, Minecraft, LootCrate, Unity, CarGurus and SimpliSafe to name just a few. None of these startups embraced the “billions or bust” mentality at the start, though many are worth billions now. Most took very little venture capital until after they proved out product/market fit and knew how they could use the money to accelerate growth. Some didn’t take any capital at all.

All were hyper-efficient in the way they used capital from Day One. Several have gone public, a few have been acquired for billion-dollar sums. I don’t fetishize bootstrapping, but there is a lot to learn by studying how these founders built huge businesses with efficient use of capital.

Smart people, dumb money

I was very happy to build and sell a startup for nearly $100 million, and while I would have liked to build a billion-dollar business, too many founders treat the probability of either outcome as close to equal. Earning billion-dollar exits is startup nirvana, for sure. But selling for $500 million is a home run, $100 million exits are amazing and $50 million exits can change the lives of families for generations. Even a “humble” million-dollar exit can make a huge difference in a founder’s life.

The point is, don’t be so quick to irrationally trade all of those options! Only trade these options when you’ve proven enough to have confidence that the future value of your company will be much higher. Capital has no insights. Don’t trade a solid business for a lottery ticket.

Irrationally raising money to scale something that doesn’t work does not result in building a big business. Founders should focus on smart growth and use VC to support that — instead of treating it like a steroid. Make efficient entrepreneurship your mantra. By all means, dream big — I’m not arguing that founders build small companies, solving small problems. If you have a legitimate need for capital, by all means raise it. But on the flip side, don’t sell your chance for success by giving up optionality and prematurely scaling burn rate in the name of fundraising glory.

Venture capital isn’t the right choice for most businesses, but when used well, it can be very powerful. Unfortunately, many VC-backed founders are using it incorrectly.

The Probable, The Possible, The Delusional

February 13, 2016

In 1961, President John F. Kennedy told a joint session of Congress that before the end of the decade, America would put a man on the moon. This was not an empty political promise to get elected, but a commitment of a sitting president boldly exposing himself to political ridicule in the face of failure.

If we can take ourselves back to that moment, it would be fascinating to analyze the probability that such a feat could be accomplished. It had never even been close to being achieved and was perceived by many to be insanely risky. It was only six weeks after the first human cosmonaut Yuri Gagarin had visited space in a short suborbital flight and three weeks after American Alan Shepard had repeated this historic milestone.

Needless to say, the odds were long and our president was far from proposing something with a highly probable outcome. Had his ambitions defied the laws of physics, our best engineering plans indicated we were decades away, or cost estimates required more capital than US GDP, perhaps it would have been delusional. Instead, history would prove that Kennedy was imaging an improbable, yet possible future.

The probable

In my short two-year stint working in corporate America, I have learned a great deal about probable outcomes. Senior executives didn’t dare propose things that were merely possible. Proposals required evidence of a high probability of success. One could derail a carefully crafted career over missing a forecast by 20 percent, let alone being a year late on launch of a product. It was unwise to take real risks and dream big in such an environment.

When planning for a new product launch, numbers and timelines were always very conservative, as it was considered irresponsible to imagine the possible but improbable upside. We were taught to keep things grounded in highly probable outcomes and, not surprisingly, rarely created any outcomes beyond conservative ones, as we were never inspired or incentivized to do so. Not surprising so few large company executives function well in the startup world.

The delusional entrepreneur will procrastinate finding that invalidating data for as long as possible, and then still be dismissive of the results.

The possible

By contrast, in startups, great outcomes are never probable. The expected return of nearly every startup at the beginning is frighteningly close to zero. In the context of my corporate experience, it seems astonishing that anyone would ever start a company. Perhaps that’s why so few corporate executives ever chose to do so. Startups only exist because their founders are willing to suspend the disbelief of the probable and instead consider what is possible.

I’ve joked that no early-stage startup should ever beat its plan; beating a plan would suggest that the founder didn’t imagine the totality of what was possible and undersold the potential of the startup.

Dreaming big is the reason so many startups will fall short of their plan and nonetheless deserve to be called successful. Falling short of the extreme of the possible can yield a very exciting business. Corporate America might fire you, but an acquirer, by contrast, might reward you with a very significant exit.

The delusional

At the other extreme from the probable approach is a very dangerous view of the world – the delusional. Some startup founders are so enthusiastic that they dream of futures that are not credible; they dismiss the need for customer feedback to validate their view; and they have no indicators that suggest they can build what they imagine.

Many things can be quickly tested, and when data invalidates a hypothesis, it is very much time to move on. The delusional entrepreneur will procrastinate finding that invalidating data for as long as possible, and then still be dismissive of the results. These founders will burn through all the money and talent he can garner, but with little or no value creation at the end.

With the probable, there would be no reason to start a company. With the delusional, there is a real risk that the founder is wasting years of his life on something that will never materialize outside of his own head. There is no truth of pre-ordained outcome when starting a company. Great founders live between these extremes in the world of the possible and inspire others to share that worldview.

They test those possibilities every day and frequently refine what they believe is possible to find a winning path. Living in the world of the possible is how we put a human on the moon and how we will imagine and create the valuable technologies and companies of tomorrow. Keep your eyes to the sky and your feet planted firmly on the ground.

When Burn Rate Outweighs Enthusiasm

January 13, 2016

Many business critics of Uber contend that the company is spending “unsustainably.” Despite that nearly all venture-backed startups burn capital unsustainably, Uber’s level of spending is viewed as particularly problematic among its naysayers. Negative press notwithstanding, Uber has now raised billions of dollars — many times over. How is this possible?

Uber’s investors, myself included, are still wildly enthusiastic about the unprecedented velocity of the company. It will be able to sustain its burn rate based on that excitement unless something surprising happens to its business, or it goes public.

It doesn’t matter whether a company’s burn rate is $10K per month or $10 million per month, companies die when their burn rates are greater than investor enthusiasm. Burn rate is a bet on the potential of a business. That bet, re-evaluated at each round of funding, is based on the belief of venture capitalists that multiples of value will be created with the money they invest in a company. Unfortunately for founders, enthusiasm can be fickle while burn rates are stubborn. The two can easily get out of sync.

Quirky is an example of what happens when a startup loses investor enthusiasm. The innovative home goods manufacturer raised huge amounts of capital, struck partnerships with GE and major retailers, and promised to disrupt the way household goods are made. Investors bought into this vision and the company hired a large team of engineers and designers, built world-class facilities and retail shops, and spent heavily on marketing.

Then products were delayed. Critics ridiculed their offerings. Their slick inventions stuck to store shelves. Expensive gambles failed to pay off. Quirky wasn’t worthless, but it no longer could justify its burn rate or sustain investor enthusiasm and ultimately died with the remains to be sold off as scraps.

The enthusiasm cycle

Founders exude enthusiasm. This enthusiasm is the currency for any startup. Co-founders join when they have drunk the Kool-Aid of the first founder. Then additional team members. Then investors. Investor pitches are inspiring and grandiose. Pitches are designed to garner enthusiasm.

Venture capital financing rounds suggest an implicit burn rate, typically intended to be invested in the startup over 12-24 months. Some basic math would suggest that for an imaginary $1.8 million financing to be burned down over 18 months, the company is spending $100K a month on average. Of course there is a curve to this burn rate that starts lower, as the company is scaling up, and finishes the period higher — more like $200K per month — which becomes the new baseline. It is this exit burn rate that needs to be sustained with new capital.

As a startup exits each financing period and needs more capital, it hits an important inflection point. Investor enthusiasm internal or external to the company hasn’t been tested in 18 months. The exit burn from the financing stage doesn’t necessarily reflect current enthusiasm. Instead it reflects the autopilot burn rate based assumptions 18 months earlier. Now the company needs to raise more money to fund at least a $200K per month burn rate (and hopefully additional growth). The key question is how enthusiastic is everyone now?

If the money invested is showing great signs of return, then enthusiasm will likely be high and the company will attract more capital with little difficulty. Unfortunately, this frequently isn’t the case. More often, money has been spent, the company has made some progress, and the results are mixed.

Given that there is a deepening curve to burn rate over the post financing period, sustaining the burn rate nearly always requires more capital than went in at the previous financing round. But because the burn rate increased to $200K/month, buying another 18 months now costs $3.6 million. Are the investors twice as enthusiastic about the company as when they wrote the last $1.8 million check? If not, the company is in trouble.

Never think of burn rate as a prescribed plan at the time of investment to be set on autopilot, and don’t assume that investors will keep funding the burn when the bank account approaches empty.

Why investors lose enthusiasm

The dream dies. Investors write checks into big dreams, which are validated by traction. If the trend line of the previous 18 months isn’t accelerating up and to the right, the excitement that generated the original investment is lost and the dream becomes a nightmare.

Founder flailing. Few startup founders are truly exceptional, and it’s hard to build an amazing startup. I’ve met many investors who are thrilled about the concept of a company, work hard with the team to make it a reality, but become frustrated by the inability of the founders to execute. Sometimes an investor will look to replace the founders in this context. Other times they’ll throw up their hands and lose interest in the startup.

Macro changes. The macro environment plays a significant role in whether investors are open-minded or close-minded to a vision of the future. The more traction a company has, the less impact the macro environment has on investor enthusiasm, but even startups with solid metrics struggle to raise money during major macro shifts, like the 2008 financial crisis. Moreover, startups that are doing well, often face down rounds in a souring economic climate.

It may be that the company had an easier time raising the previous round because the investor confidence in the macro environment made it possible for investors to dream along with the founders, and by the time the company is out for more capital, that environment has shifted. It is hard to dream big dreams when the prevailing economic sentiment is fear.

During the 2008 financial crisis, companies that were funded 12-18 months before and had solid metrics struggled to inspire enthusiasm from fearful investors. Sometimes the shift is less dramatic, and a single sector will fall out of favor. I think many early-stage e-commerce companies are feeling this squeeze right now, where investor enthusiasm for e-commerce was much stronger a couple years ago.

What to do if enthusiasm wanes

Should the startup search for external money without strong internal support? This rarely works out. Outside investors are always trying to read the tea leaves to understand how insiders feel, as they have way more insight into the company and leadership.

So how can a company manage the enthusiasm challenge? Keep a very close eye on the disconnect between burn rate and enthusiasm. Never think of burn rate as a prescribed plan at the time of investment to be set on autopilot, and don’t assume that investors will keep funding the burn when the bank account approaches empty. It’s the founder’s job to drive enthusiasm for more financial support by building traction in the business and not burning ahead of that enthusiasm.

Remember that the burn rate represents the plan from a moment of high enthusiasm and that the enthusiasm may or may not sustain. The key question is whether the investors would still write their check, if given the choice, as time passes and the burn increases. Are they as excited today as when they wrote the last check? If not, don’t hit the gas; perhaps even back off the burn. Find some metric and make it grow fast. Nothing sparks enthusiasm like momentum. Seek out kindred investors who are willing to back your audacious vision through a tough macro turn.

Don’t let your most enthusiastic supporters burn out. That’s how startups die.

The Platform Paradox

November 28, 2015

I often hear VCs say that they don’t back products, they back platforms. I find that logic backwards and in many ways dangerous for founders. Platforms can provide a durable competitive advantage, and it’s easy to understand why startups would want to create one. But great platforms are nearly always born from companies first creating great products with narrow, but compelling use cases.

Founders have a hard time accepting this advice, because they hear that VCs only want to back businesses with unicorn potential. They have difficulty imagining that a niche point solution could fit the bill. So they dream up a story of how their startup could become a platform and lose focus on the problem they’re solving.

The Difference Between A Platform And A Product

Given all the discussion of platforms, networks, marketplaces and horizontal strategies, it’s surprising that more hasn’t been written defining and delineating these terms. Before I explain why entrepreneurs should ignore the platform logic, I will do my best to provide definitions to these different concepts. I do not consider these definitions to be comprehensive and am open to engaging with anyone who thinks about these concepts differently.

Products

Products are tools or services that you have some exclusive ownership of or access to. iPhones and GoPros are products. Microsoft Office and Adobe Photoshop are products. Candy Crush and The New York Times mobile app are products.

You might pay a flat price, a SaaS fee, trade your attention for ads, get some amount of free usage or partake in in-app purchases, but the concept is the same. You buy or sign up for something and use it. A good product solves a specific need for the user whether a trivial utility or a practical one.

Platforms

Amazon Web Services, iOS and Android are platforms. The distinguishing aspect of a platform is the ability for others to build products and ultimately generate revenue on top of it, often in ways the platform creator never imagined. Platforms generate revenue by taking a cut of proceeds, and costs tend to scale in proportion to their use.

Networks

People often confuse “platforms” with products that posses network effects, but they are different things. LinkedIn is a network, that later became a platform for recruiting. Pinterest is a beautiful interest graph and not a development platform, yet it is becoming a platform for advertising as it grows. Both services offer APIs, but an API does not a platform make.

Marketplaces like eBay, Airbnb and Etsy are networked products that feel like platforms because you can make money using them, but limit the ways you can use them. I can’t sell a car on Airbnb or rent a castle on eBay. The primary value in marketplaces is derived from the liquidity. You’re not building value on top of these networks, you’re exchanging value within them.

There is value to be created on the margins of these services — listing management tools for eBay power sellers, or home cleaners for Airbnb hosts — but the primary value creation accrues to the company who creates the network. Airbnb is no more a platform for housekeepers than a high rise office building is.

Reasonable people can disagree with these definitions. For instance, each of these companies is a “product” company of one sort or another. But they at least clarify some major distinctions.

Humor VCs When They Bring Up Platforms

Most VCs have never built companies and some do not fully appreciate the challenges of doing so. Founders may have a great idea for a startup that would solve a real problem. There may even be a clear revenue model, but the founders fear that it all sounds too small. Instead of touting their product, founders dream up some abstract notion that combines a multibillion-dollar Total Addressable Market (TAM) that applies tech in some incredibly bold, yet ambiguous way.

VCs start by looking at the billion-dollar platform idea and want to believe that you’ll birth your company to achieve the end state on day one. There is nothing wrong with painting the big picture of what your company will become over time, but make sure those VCs know that you’re going to start by solving a real problem for customers and that you’re going to build a product now that hopefully can become a platform over time. Most importantly, tell them you’re not going to get distracted building a grandiose platform that no one wants today.

This is how platform logic becomes dangerous. When specs are broad enough to apply to many different customers, they often work well for no one. Product managers dabble with small customizations, but try to preserve the breadth to do anything. Horizontal platforms leave startups waiting for markets to come to them. That can take a long time. It usually never happens.

Narrow, vertical product use cases often seem insignificant compared to the promise of a platform. Unfortunately, products and platforms are mutually exclusive at early-stage startups. It is nearly impossible to offer a high-quality use case while also being a platform.

When I hear founders who barely have a demo talk about their “platform play,” I hear a founder without a clear grasp of their customers’ needs. Abstraction lends itself to grand pronouncements, but is usually so general as to be unactionable.

At that point I ask about how the platform will reach critical mass. What follows is invariably hand-waving of some sort. The marketing plan usually involves a few key influencers and a hodge-podge of unquantifiable marketing programs, but it is nearly impossible to build critical mass when no one understands what specific problem you’re solving.

Having a big vision is usually a good thing unless it becomes a huge distraction. To become a platform you first need to build a product that speaks to a compelling use case.

Build a Single Player Mode

If you’re stuck on the notion of building a platform, at least devote time to developing a credible “Single Player Mode.” Whatever you build should offer value even if only one person signs up. Instagram helps people take better photos, and the network comes afterward. Pinterest can serve as a mood board for crafters; the connections it enables turn it into a sewing circle with global scale. Minecraft is like the world’s biggest LEGO set, and an Internet connection turns it into the world’s biggest playgroup.

Don’t Trust Me—Study Bezos, Zuckerberg, and Jobs

Platforms can be compelling businesses, but it’s nearly impossible for a startup to create one from scratch. Remember when Google tried to build a Glass Collective (imitation is the greatest form of flattery) with support from A16Z and Kleiner Perkins, but still ended up killing the project? Ultimately Google should have prioritized building a compelling product rather than building a platform for a product nobody wanted.

The reality is that most platforms in the startup world emerge as the byproduct of a successful product solution. Amazon’s AWS, Facebook and iOS are arguably three of the most important platforms in tech today, but each company entered the platform business somewhat unwittingly.

Amazon

Amazon Web Services (AWS) has become a core part of the startup infrastructure and has probably been the single-most important innovation responsible for the explosion of startups since the formalization of the HTTP standard.

But remember, Amazon didn’t set out to build a generic computing infrastructure platform, they sold Harlequin romance novels, DVD box sets of Lost, tennis rackets and millions of other products.

It wasn’t until they mastered the grubby art of shipping and receiving that they turned their attention towards computing services. Their platform was the byproduct of a much loved and trusted point solution, not the company’s focus.